In 2024, the global economy presented a varied landscape of recovery and challenges across different regions. The United States experienced uneven growth, with a sluggish start in the first quarter, a rebound in the second, and a slowdown in the third, influenced by global economic adjustments and high-interest rates. Inflation eased somewhat, prompting the Federal Reserve to cut rates to support growth. In China, economic growth slowed due to weak demand and a struggling property sector, despite government efforts to stimulate recovery. Meanwhile, the UK showed signs of recovery, supported by rising wages and reduced inflation, while the Eurozone witnessed its strongest growth in two years, driven by improved performances in France and Spain.

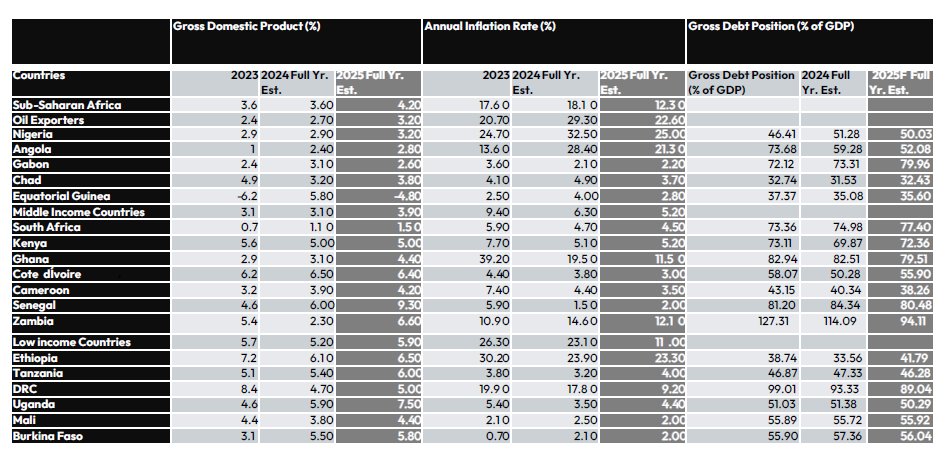

Sub-Saharan Africa saw mixed outcomes in 2024, with countries like South Africa and Kenya dealing with political and economic challenges, while Ghana and Ivory Coast achieved growth through resource exploitation. Inflation rates varied across the region, influenced by both local and global factors.

2025 Global Review

Looking to 2025, the global outlook appears cautiously optimistic, with projected GDP growth of 3.30%. This growth is expected to be led by emerging markets, likely outpacing advanced economies. Inflation is anticipated to moderate further, with advanced economies seeing rates closer to pre-pandemic levels. Central banks are expected to continue adjusting interest rates to strike a balance between economic growth and inflation. Key challenges such as structural issues in advanced economies and potential geopolitical tensions, particularly involving Russia and Ukraine, will play a significant role in shaping the economic landscape.

In Sub-Saharan Africa, 2025 offers potential for stronger growth driven by increased private consumption and investment, though challenges like high debt and political instability remain. Inflation in the region is expected to decline but stay above pre-pandemic levels.

GDP Growth: India led with strong growth (7.80% in Q1 and 5.40% in Q3-2024), while Germany and Japan saw negative or stagnant growth. Inflation: India saw a higher inflation of 6.20%, US, UK, and Euro Area recorded modest decline from Q1 to Q4, while China and Japan stood out with lower inflation rate. Interest Rates: Generally, interest rates declined across most advanced economies, with the U.S. and UK seeing significant reductions. Debt Levels: Advanced economies like France and Canada have the highest debt-to-GDP ratios, exceeding 900.00%, while India and South Korea maintained relatively low levels. Unemployment: Unemployment rates in the advanced economies were mixed, with some countries experiencing a slight increase and others a decrease.

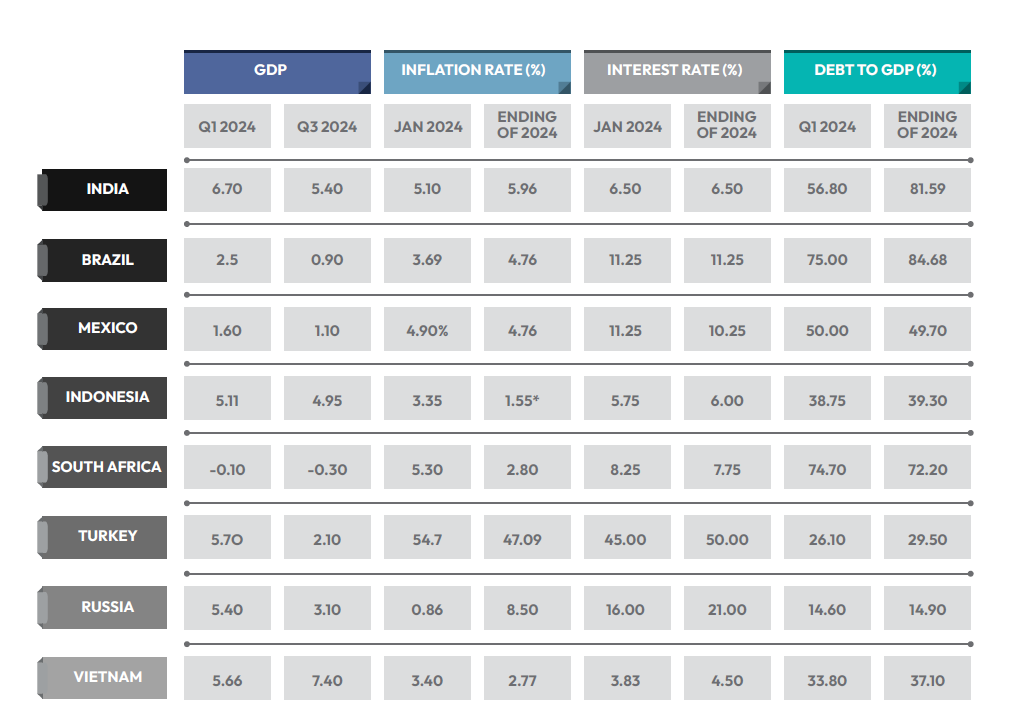

GDP Growth: In 2024, GDP growth in emerging economies was mixed with India and Vietnam showing robust growth, while South Africa experienced a contraction. Brazil and Mexico show moderate growth. Inflation: Inflation remained elevated across most emerging economies with Turkey and Russia having the highest rates. Indonesia and Vietnam stood out with lower inflation rates. Interest Rates: Interest rates decisions across central banks were mixed as Indonesia, Turkey, Russia, and Vietnam saw interest rate hikes, while, Mexico and South Africa recorded interest rate cuts but India and Brazil maintained their interest rates. rates, and ongoing geopolitical uncertainty. While some countries showed signs of resilience, others struggled with economic headwinds.

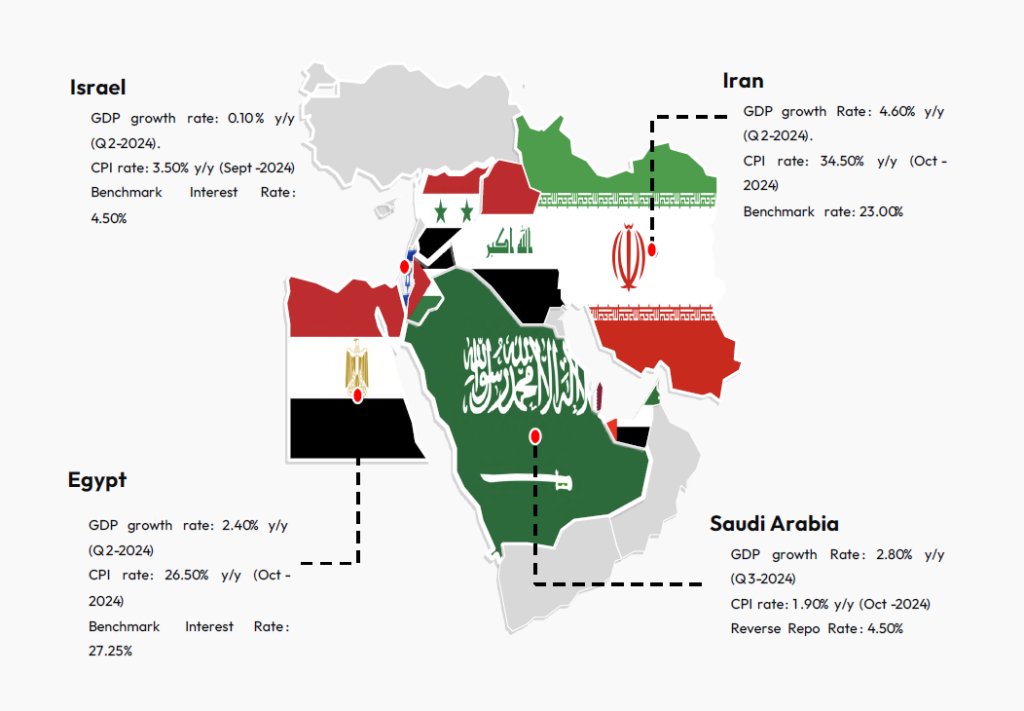

MIDDLE EAST: GULF COOPERATION COUNCIL SUPPORTED ECONOMIC GROWTH

The Gulf states have relied on their abundant hydrocarbons, particularly oil, to pursue economic and political activities that serve their national interests. The foreign and domestic policies of the Gulf Arab countries (Bahrain, Kuwait, Oman, Qatar, Saudi Arabia and the United Arab Emirates, or UAE) significantly affect global energy security, international stability and global markets. The region holds more than 30.0% of the world’s proven crude oil and 20.0% of its natural gas reserves.

Real GDP growth in the Middle East has been modest in 2024. Most of the growth has been driven by Gulf Cooperation Council (GCC) countries. According to the World Bank’s Gulf Economic Update, economic growth in the GCC is expected to grow by 2.80% in 2024 and 4.7% in 2025. The region’s prospects builds on the strong momentum of the non-oil economy, and the recovery in oil output.

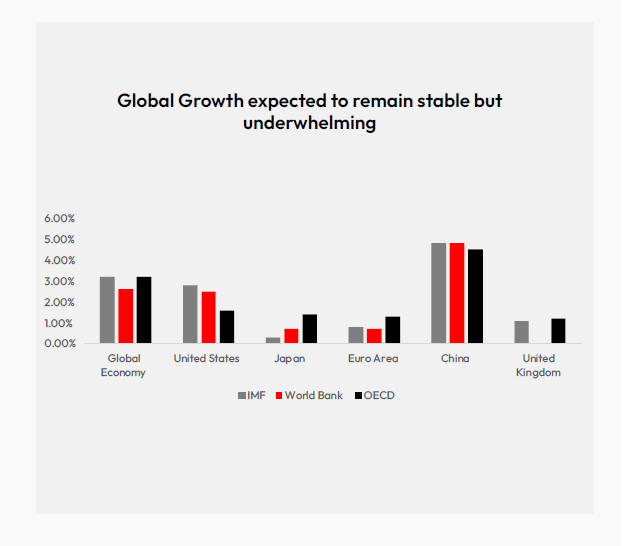

GLOBAL FORECASTS: GLOBAL GROWTH TO REMAIN STABLE BUT SLIGHTLY UNDERWHELMING

Global output will moderate slightly to 3.20% in 2024 and 2025

compared to 3.30% in 2023.

This is due to the concerns that continued geopolitical uncertainties, particularly around trade relations, energy supplies, and geopolitical risks in Eastern Europe and the Middle East, may hinder global trade flows and investor confidence, limiting overall output growth.

Many countries are winding down the fiscal support measures that were implemented during the pandemic and global energy crisis. As these supports phase out, public spending will contribute less to GDP growth, particularly in

developed economies.

Trump’s tariff policies will reduce

global GDP as global trade and

investments may be affected due to uncertainties, cut down in trade volumes, and restructured supply

chain.

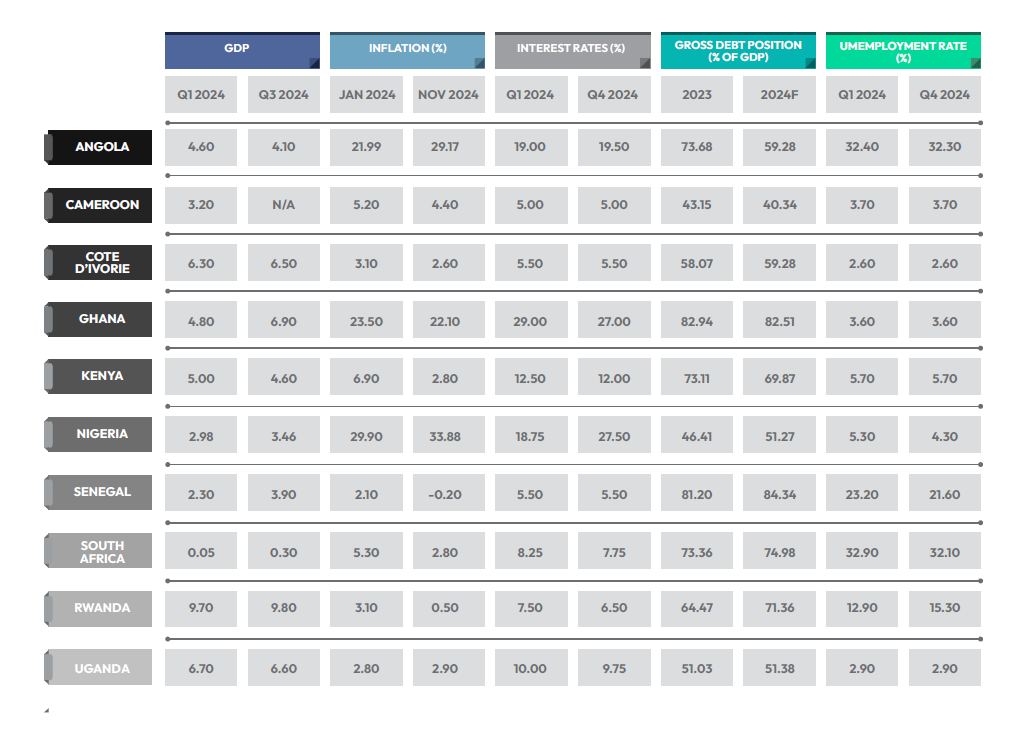

GDP Growth: Sub-Saharan Africa witnessed a mixed growth with Rwanda, Ghana, Uganda and Cote d’voire showing robust growth, while South Africa experienced a slight contraction. Most other countries showed moderate growth.

Inflation: Inflation remained elevated across most SSA countries, with Nigeria, Ghana, and Angola having the highest inflationary pressure. Cote d’Ivoire, Rwanda, and Uganda stood out with lower inflation rates.

Interest Rates: Central banks tightened monetary policy rates as inflationary pressure became stubborn across the board. Nigeria, Ghana, and Angola recorded the highest interest rates in 2024.

In 2025, Sub-Saharan Africa’s growth is projected to improve to 3.60%, driven by easing inflation, increased private consumption, and investment. However, risks such as geopolitical tensions, regional instability, and economic slowdowns in China pose significant threats to this outlook.

Nigeria (3.20%): Modest growth will be driven by oil production recovery. However, persistent challenges like insecurity and fiscal imbalances constrain faster growth.

Angola (2.80%): Growth reflects stabilized oil production and reforms but faces vulnerabilities from external oil price fluctuations.

South Africa (1.50%): Slow growth due to structural issues like energy shortages, high unemployment, and policy uncertainties.

GDP FORECAST: THE NIGERIAN ECONOMY TO MAINTAIN A STEADY GROWTH PERFORMANCE

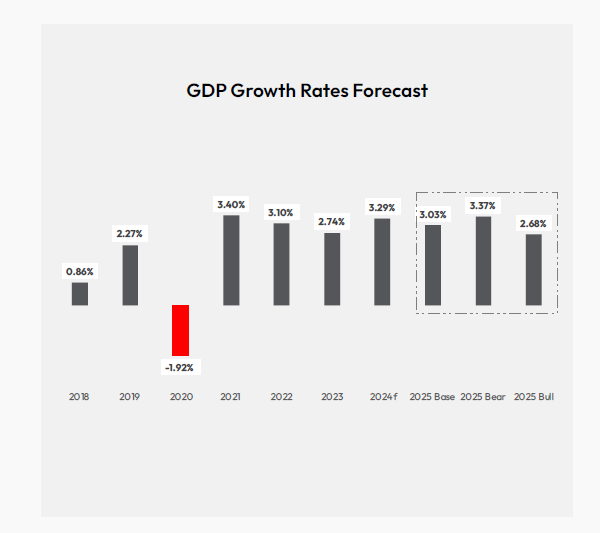

The Nigeria’s GDP will maintain its steady growth in 2025, driven by a sustained rebound in the oil sector and slow but steady growth in the non-oil sector. We project that Nigeria’s real GDP will increase modestly to 3.03% in 2025.

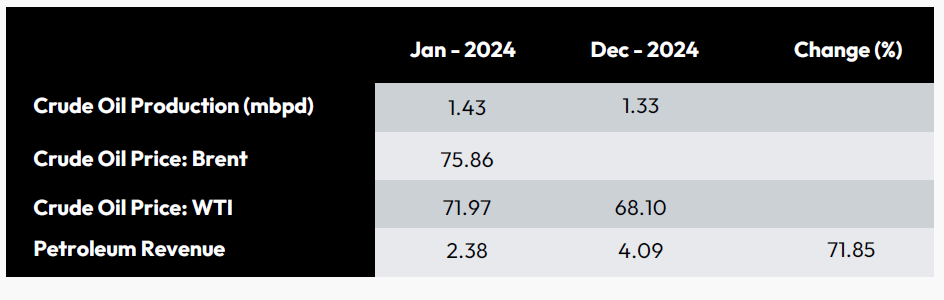

In the oil sector, the Nigerian economy is set to benefit from favourable developments, as evidenced by 2024 performance. Net exports are expected to be the primary growth driver, with rising oil export volumes due to improved security in the Niger Delta, commencement of production at Port Harcourt Refinery, and increased production from Dangote refinery displacing most of the fuel and chemical imports in 2025.

Objectives: To provide steady returns, align with market performance, and ensure low portfolio turnover.

Common Investments: Broad market index funds (like S&P 500 ETFs), large-cap stocks, or diversified bond funds.

Recommendable Free Float: For a company to qualify as a core holding in a portfolio, a recommendable free float is generally above 50.00%. This is because a higher free float is beneficial for core portfolio holdings to ensure portfolio liquidity & stability and reduced volatility. Also, these stocks often have heightened market confidence.

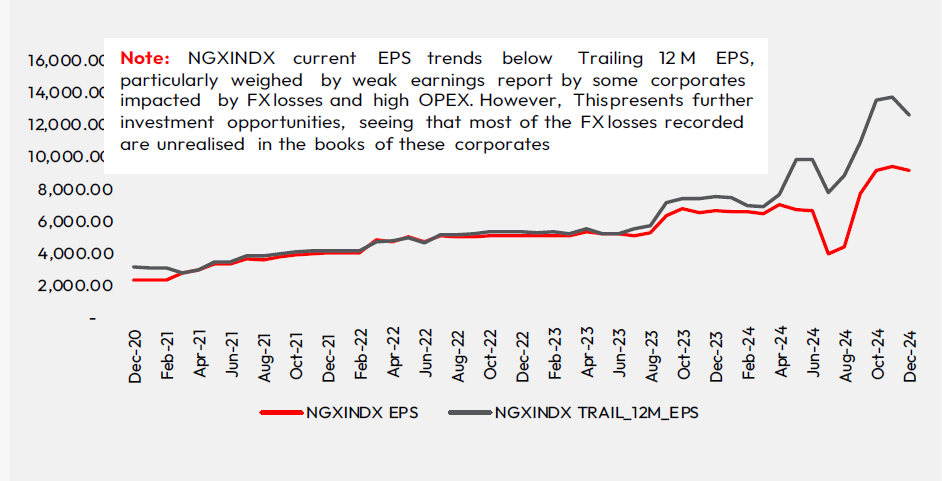

NGX Index Current EPS vs Trailing 12M EPS

Objectives: To enhance the portfolio’s returns by capturing specific market trends or taking advantage of short-term opportunities.

Common Investments: Sector-specific funds, small-cap stocks, emerging markets, growth stocks, or alternative assets (like REITs or commodities).

Recommendable Free Float: For a company to qualify as a core holding in a portfolio, a recommendable free float ranges between 20.00% and 50.00%. Because satellite holdings tend to be more volatile or niche investments, the moderate free float range ensures liquidity for opportunistic trades.

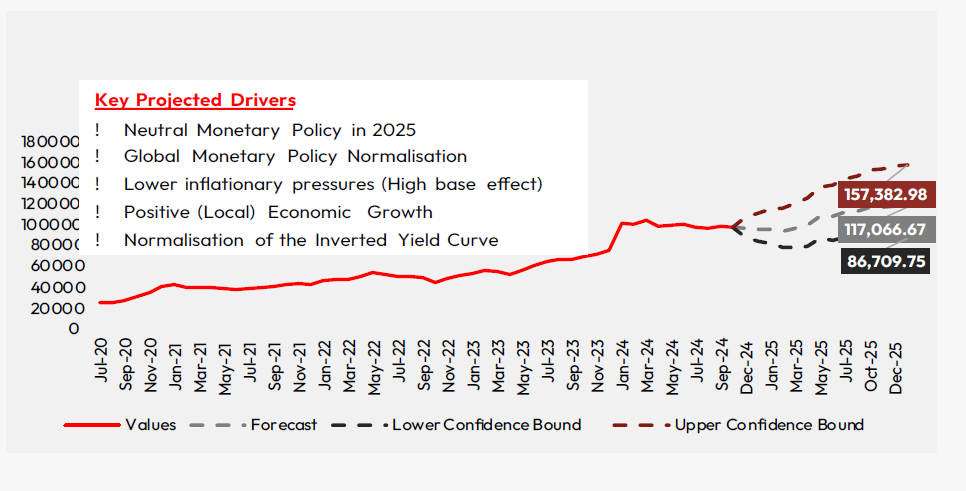

Investors interest towards duration exposure was lacklustre for the better part of 2024

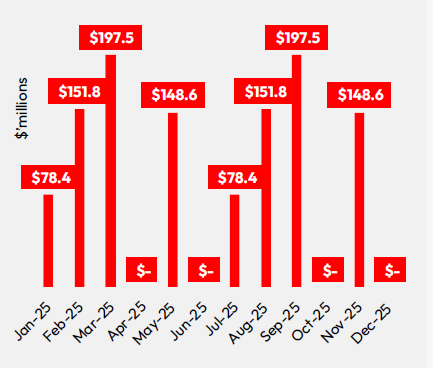

Total Offer vs Total Subscription vs Total Sales at DMO Auction

The market for sovereign duration-exposed instruments (“long-dated bonds”) was relatively quiet in 2024 (particularly at the secondary market), given the elevated level of short-term duration instruments in the same period.

Uncertainty surrounded bond supply in H1-2024 due to irregular auction calendars. The FG conducted sporadic bond auctions in H1-2024, raising 85.0% (N4.67trn) of the total amount (N5.48trn) raised in 2024. The proceeds from the bond auctions conducted were used for budgetary support and clearing out a significant portion of FG’s outstanding Ways and Means with the CBN.

Ultimately, factors that drove bond yields/prices in 2024 include: supply and demand fundamentals, system liquidity, and MPR movements.

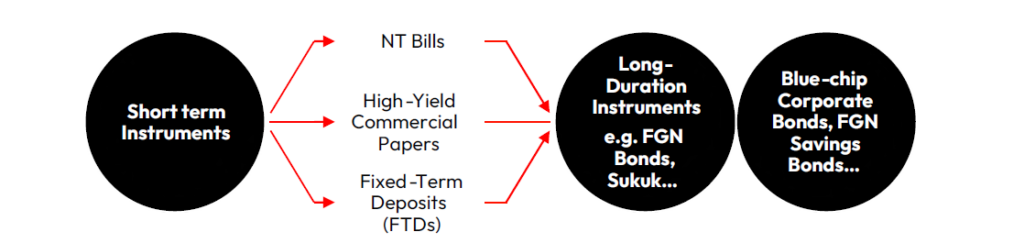

STRATEGY: BARBELL STRATEGY WITH TACTICAL ALLOCATION

Barbell Strategy with Tactical Allocation: Brief Summary

This strategy is fortified to leverage the high yields of short-term instruments, while positioning for future gains on long duration bonds. It seeks to strike a balance between income generation, stable liquidity, and portfolio growth.

We use cookies to ensure that we give you the best experience on our website. By clicking "Accept", you agree to our Cookie Policy. AcceptPrivacy Policy

Manage consent

Privacy Overview

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. These cookies ensure basic functionalities and security features of the website, anonymously.

Cookie

Duration

Description

cookielawinfo-checkbox-analytics

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics".

cookielawinfo-checkbox-functional

11 months

The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional".

cookielawinfo-checkbox-necessary

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary".

cookielawinfo-checkbox-others

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other.

cookielawinfo-checkbox-performance

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance".

viewed_cookie_policy

11 months

The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data.

Functional cookies help to perform certain functionalities like sharing the content of the website on social media platforms, collect feedbacks, and other third-party features.

Performance cookies are used to understand and analyze the key performance indexes of the website which helps in delivering a better user experience for the visitors.

Analytical cookies are used to understand how visitors interact with the website. These cookies help provide information on metrics the number of visitors, bounce rate, traffic source, etc.

Advertisement cookies are used to provide visitors with relevant ads and marketing campaigns. These cookies track visitors across websites and collect information to provide customized ads.