In 2024, the global economy presented a varied landscape of recovery and challenges across different regions. The United States experienced uneven growth, with a sluggish start in the first quarter, a rebound in the second, and a slowdown in the third, influenced by global economic adjustments and high-interest rates. Inflation eased somewhat, prompting the Federal Reserve to cut rates to support growth. In China, economic growth slowed due to weak demand and a struggling property sector, despite government efforts to stimulate recovery. Meanwhile, the UK showed signs of recovery, supported by rising wages and reduced inflation, while the Eurozone witnessed its strongest growth in two years, driven by improved performances in France and Spain.

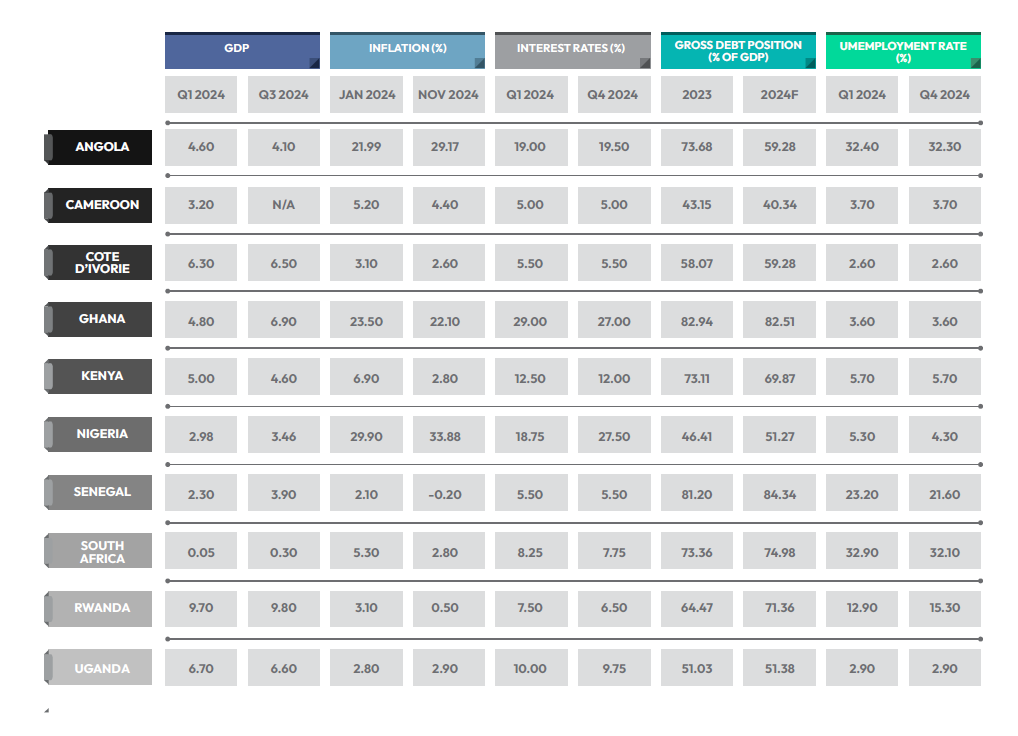

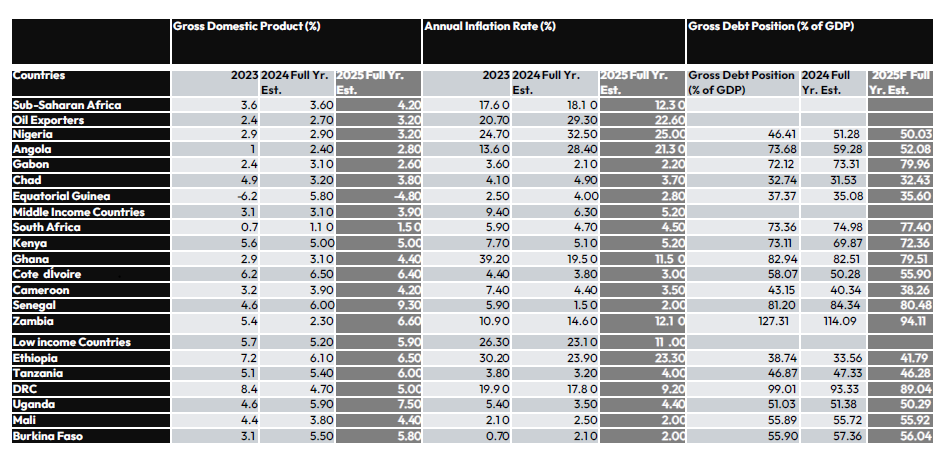

Sub-Saharan Africa saw mixed outcomes in 2024, with countries like South Africa and Kenya dealing with political and economic challenges, while Ghana and Ivory Coast achieved growth through resource exploitation. Inflation rates varied across the region, influenced by both local and global factors.

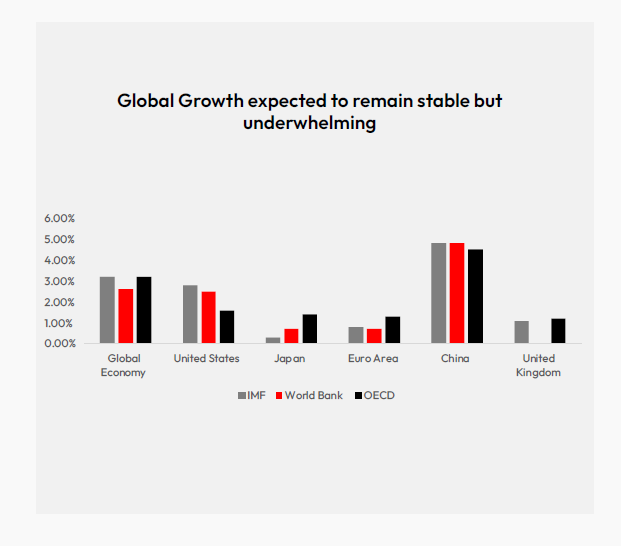

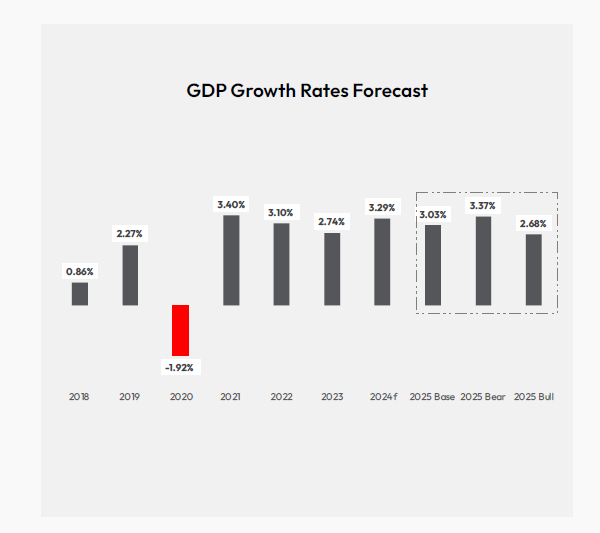

Looking to 2025, the global outlook appears cautiously optimistic, with projected GDP growth of 3.30%. This growth is expected to be led by emerging markets, likely outpacing advanced economies. Inflation is anticipated to moderate further, with advanced economies seeing rates closer to pre-pandemic levels. Central banks are expected to continue adjusting interest rates to strike a balance between economic growth and inflation. Key challenges such as structural issues in advanced economies and potential geopolitical tensions, particularly involving Russia and Ukraine, will play a significant role in shaping the economic landscape.

In Sub-Saharan Africa, 2025 offers potential for stronger growth driven by increased private consumption and investment, though challenges like high debt and political instability remain. Inflation in the region is expected to decline but stay above pre-pandemic levels.

GDP Growth: India led with strong growth (7.80% in Q1 and 5.40% in Q3-2024), while Germany and Japan saw negative or stagnant growth. Inflation: India saw a higher inflation of 6.20%, US, UK, and Euro Area recorded modest decline from Q1 to Q4, while China and Japan stood out with lower inflation rate. Interest Rates: Generally, interest rates declined across most advanced economies, with the U.S. and UK seeing significant reductions. Debt Levels: Advanced economies like France and Canada have the highest debt-to-GDP ratios, exceeding 900.00%, while India and South Korea maintained relatively low levels. Unemployment: Unemployment rates in the advanced economies were mixed, with some countries experiencing a slight increase and others a decrease.

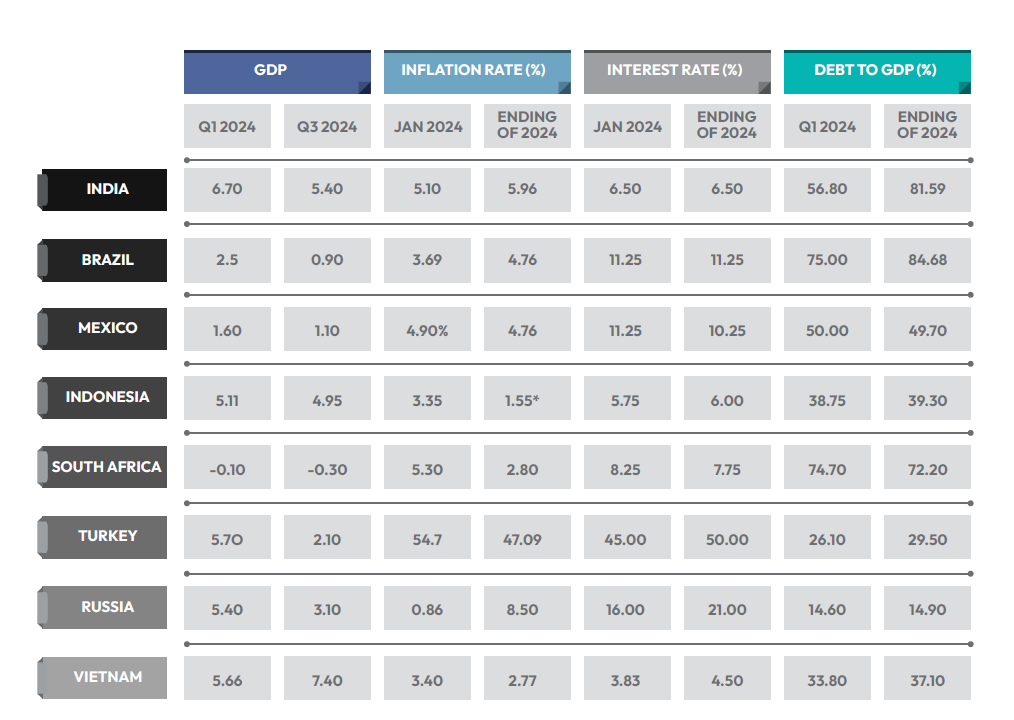

GDP Growth: In 2024, GDP growth in emerging economies was mixed with India and Vietnam showing robust growth, while South Africa experienced a contraction. Brazil and Mexico show moderate growth.

Inflation: Inflation remained elevated across most emerging economies with Turkey and Russia having the highest rates. Indonesia and Vietnam stood out with lower inflation rates.

Interest Rates: Interest rates decisions across central banks were mixed as Indonesia, Turkey, Russia, and Vietnam saw interest rate hikes, while, Mexico and South Africa recorded interest rate cuts but India and Brazil maintained their interest rates.

Debt Levels: Debt levels continue to rise in most emerging countries with India and Brazil having the highest levels. However, South Africa recorded a slight decline in its debt level, howbeit still high at 72.20%.

Overall: The emerging market economies faced a challenging environment with persistent inflation, rising interest rates, and ongoing geopolitical uncertainty. While some countries showed signs of resilience, others struggled with economic headwinds.

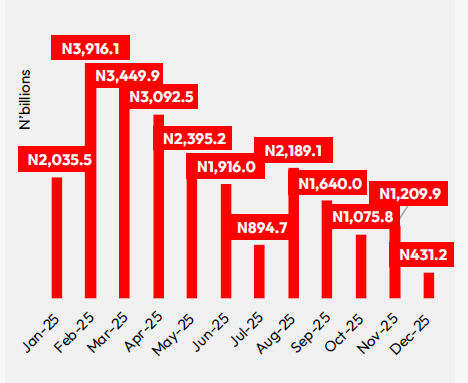

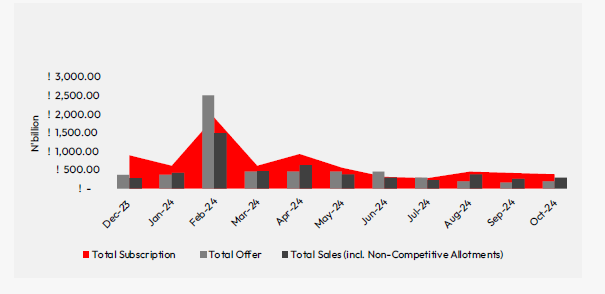

Uncertainty surrounded bond supply in H1-2024 due to irregular auction calendars. The FG conducted sporadic bond auctions in H1-2024, raising 85.0% (N4.67trn) of the total amount (N5.48trn) raised in 2024. The proceeds from the bond auctions conducted were used for budgetary support and clearing out a significant portion of FG’s outstanding Ways and Means with the CBN.

Ultimately, factors that drove bond yields/prices in 2024 include: supply and demand fundamentals, system liquidity, and MPR movements.

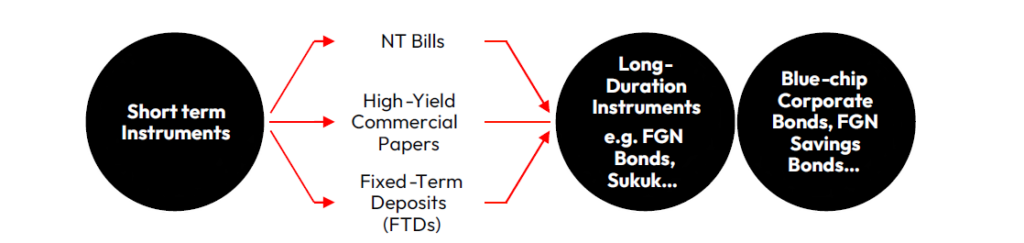

This strategy is fortified to leverage the high yields of short-term instruments, while positioning

for future gains on long duration bonds. It seeks to strike a balance between income generation,

stable liquidity, and portfolio growth.